iPhone on EMI vs Cash: The Harsh Financial Reality for Our Youth

Walk into any coffee shop in Delhi, Mumbai, or Bangalore, and you will see a familiar sight: a table full of young professionals, barely in their first or second job, placing their iPhone Pro Max models face down on the table. It has become a modern ritual. The three-camera array isn’t just a piece of technology anymore; it is a social currency.

But beneath the shiny titanium finish lies a harsh economic reality. While we love to emulate the lifestyle of the West, there is a fundamental difference in how they acquire these gadgets versus how we do.

Let’s break down the “iPhone Gap” and understand why buying a premium phone on a 24-month EMI might be a financial Galti / Mistake that is keeping Indian youth from building real wealth.

1. The Economic Reality Check: Days of Work Required

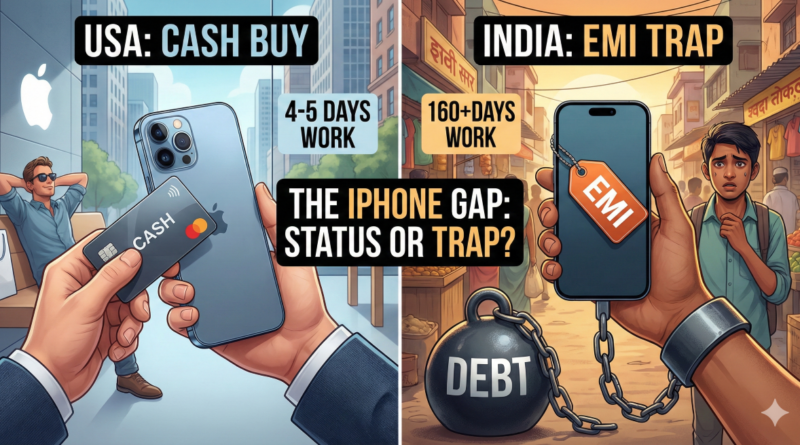

To understand the gravity of the situation, we need to move beyond the price tag and look at “Time Value.” How much of your life (in working days) do you have to trade to own that device?

Let’s take a standard iPhone Pro Model (approx. $1,000 – $1,200). In India, due to taxes, this translates to roughly ₹1,30,000 to ₹1,40,000.

Here is a comparison of how many days an average citizen needs to work to pay off this device fully:

| Country | Avg. Daily Income (Approx.) | iPhone Cost (Local) | Days of Work Needed |

| USA | $240 (₹21,600) | ~$1,099 | 4 – 5 Days |

| UK | £153 (₹17,100) | ~£999 | 6 – 7 Days |

| China | ¥450 (₹5,600) | ~¥8,999 | 20 – 25 Days |

| India | ₹850 ($9.4) | ₹1,34,900 | 158 – 160 Days |

***Believe it or not, I have increased our daily income to over 200-250 INR

The “One Week” vs. “Half Year” Gap

For an American, buying an iPhone is like an Indian buying a mid-range pair of sneakers. It is a casual purchase. It doesn’t affect their rent, their food, or their savings.

For an average Indian youth, that same phone costs nearly half a year’s worth of labor. When you buy it on EMI, you aren’t just paying money; you are mortgaging your future freedom. You are entering a cycle of Udhaar/Debt or Loan just to look like you belong to a tax bracket you haven’t reached yet.

2. The Psychology: Utility vs. Show-off

Why do we do it? In the US and UK, the iPhone is arguably the most common phone. A CEO uses it, and so does the intern. It is seen as a utility tool – reliable, simple, and functional.

In India, however, the purchase is often driven by Bhed-chaal / Herd Mentality. We see our friends upgrading, we see influencers flaunting unboxings, and we feel the pressure to conform. The “No-Cost EMI” schemes offered by banks are designed to exploit this specific psychological trigger. They break down a massive, unaffordable sum into small, digestible chunks (e.g. ₹5500/month).

But ask yourself: Is paying ₹5500 every month for two years essentially “renting” a lifestyle you cannot afford? That money could have been a SIP (Systematic Investment Plan), a fund for a solo trip, or capital for a small side business.

3. The Law of Diminishing Returns: When All Phones Become the Same

There is a massive tech secret that companies don’t want you to think about: The plateau of performance.

Ten years ago, a ₹15000 phone was garbage, and a ₹60000 phone was amazing. Today, the gap has closed significantly.

Speed: Does Instagram open faster on an iPhone 17 Pro than on a OnePlus or a Nothing Phone? Not really.

Display: Most mid-range phones now have 120Hz OLED screens.

Battery: Many Androids actually charge faster and last longer.

At a certain level (usually around the ₹25000 – ₹35000 mark), the phone becomes “good enough” for 99% of users. Anything you spend above that is largely for brand value and minor camera improvements that are invisible on social media compression. Buying a flagship just to scroll Reels is purely a Shauq/Hobby or Desire without logic.

4. Purpose-Driven Purchasing

This brings us to the most critical point: Purpose.

A phone is a tool. In the hands of a creator, a videographer, or a business owner who manages operations from their device, a premium phone is an investment. It generates ROI (Return on Investment).

If you are a YouTuber shooting 4K vlogs, the iPhone is an asset.

If you are a student or a salaried employee with a desk job, the Pro or Max is likely a liability.

We need to stop making decisions based on features we might use (“What if I shoot a movie one day?”) and start making decisions based on our actual Zaroorat / Need.

📊 The Tech-Life Balance Sheet: How Much Should You Actually Spend?

Use this simple “Salary-to-Phone” calculator to find your safe zone. The rule is simple: Never go broke looking rich.

🛑 The 3 Golden Rules of Buying

The “General User” Rule (50% of Monthly Salary): If you use your phone only for WhatsApp, Calls, Instagram scrolling, and YouTube watching, you should never spend more than half of your monthly take-home salary on a phone.

Why? Because it is a depreciating liability. It loses value the moment you open the box.

The “Enthusiast” Rule (100% of Monthly Salary): If you are a heavy gamer (Wuthering Waves / any esports game ), a tech geek, or someone who uses their phone for 6+ hours a day for intense tasks, you can stretch your budget to equal one month of your salary.

Condition: You must pay in Rokda / Cash. No EMIs allowed here.

The “Creator/Pro” Rule (The ROI Exception): If you are a content creator (YouTuber, Instagram Influencer) or run a business from your phone, the device is an Auzaar / Tool or Assest. In this case, you can spend up to 1.5x to 2x your monthly income, only if that phone improves your video quality or workflow enough to help you earn more money back.

🧠 The “EMI Test”

Before you click “Buy Now” on EMI, answer these three questions honestly:

If my phone breaks tomorrow, can I buy a new one immediately with cash?

If No: You cannot afford the phone you are holding.

Will this phone help me earn the EMI amount back every month?

If No: It is a bad investment.

Am I buying this for features or for status?

If Status: Remember, wealthy people stay rich by living like they are poor. Poor people stay poor by acting like they are rich. Use your Samajhdaari / Wisdom.

Conclusion: Don’t Be “Phone Rich, Cash Poor”

The West buys these phones with cash because, for them, it is a tiny fraction of their wealth. When we buy them on EMI, we are trying to sprint before we can crawl.

There is no shame in using a budget phone. In fact, there is a quiet confidence in knowing your bank account is growing while your phone is simple. Let’s stop falling for the marketing hype.

The Golden Rule: If you cannot buy it twice in cash without stressing about your rent, you cannot afford it. Don’t let a gadget become a Bojh / Burden on your peace of mind.